Suppliers have to calculate very carefully, especially when the economy is weak. The right quotation calculation helps to correctly determine and cover costs, as well as to win lucrative orders with competitive prices.

Due to the extreme price and cost pressure on suppliers, more and more companies have expanded their costing expertise. In addition to the traditional overhead calculation at full costs, which can lead to considerable price distortions, they are now increasingly relying on process cost flat rates and, in parallel, on relative contribution margin accounting. However, this transparent calculation method is based on the strict separation of full and partial costs. As a result, those responsible for pricing can see which of their parts still yield enough margin and where the lower pain threshold is in price negotiations.

© THIELEN SOFTWARE & CONSULTING

Calculating large and small batch sizes correctly

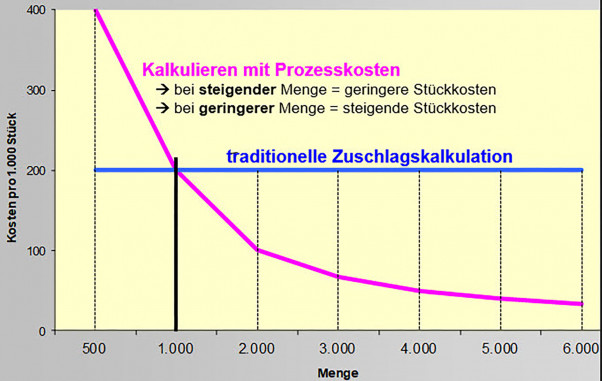

The disadvantages of classic overhead costing are obvious: due to rigid, percentage-based overhead surcharges on the individual cost values, the method quickly leads to an excessive price increase when production quantities increase. Conversely, the procedure can lead to subsidized prices when calculating smaller production lot sizes. The alternative method of applying process costs – known internationally as “ABC” (Activity-Based Costing) – leads to a degression in unit costs as batch sizes increase, as the diagram shows.

However, overhead costing extended to include process costs is no guarantee of acquiring lucrative orders. This is because there are an increasing number of calculators who prefer relative contribution margin accounting. This means that they also take into account the time required for production throughput and administration.

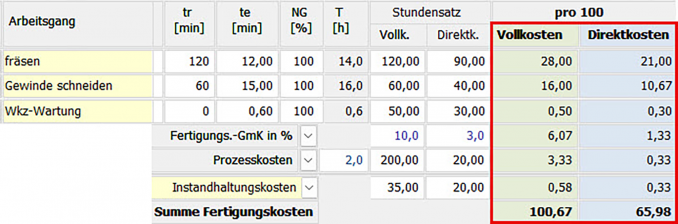

Companies that are considering changing their costing method due to price pressure are advised by Sauerland-based management consultant Peter Thielen to proceed with caution. In his many years of experience, he has advised numerous companies to use “parallel costing”. In this method, the full and partial costs are directly compared to determine the price (see Table 1): In the left-hand column are the results of the overhead calculation at full costs, and in the right-hand column next to it are the partial costs, referred to here as direct costs.

Parallel calculation helps with price determination

The Managing Director of Mühlhause GmbH in Velbert, Dirk Mühlhause, is convinced by this parallel cost analysis: “The parallel application of overhead and contribution margin costing sustainably strengthens our decision-making reliability in pricing. Andreas Müller, Managing Director of Buerstätte in Wetter, argues similarly: “The precise determination of material costs and the evaluation of all process steps enable us to calculate more accurately and thus provide a reliable basis for our pricing.”

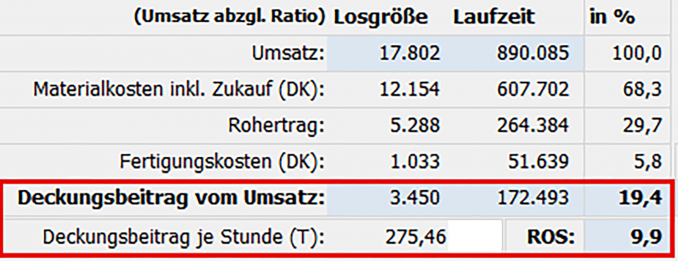

The Calcstar calculation software developed by Peter Thielen also shows how high the actual profit contribution of each individual product is. The product-specific “contribution margin per production hour” – also known as the “speed factor” – is shown in every calculation (see Table 2).

This allows Calcstar users to see at a glance whether all costs are covered in a quotation and how high the contribution margins are. “Calcstar is therefore an indispensable tool for suppliers to survive on the market even under tough competitive conditions,” summarizes Peter Thielen.

Practical tip

The REFA Association, which sets standards in German industry with regard to work organization, time management and cost accounting, offers a seminar on cost calculation. You can find further information at: www.refa.de/ausbildungen/refa-kostencontroller/kostenkalkulation-fuer-die-auftragsabwicklung

Web:

www.thielen.biz